64000 a Year is How Much an Hour? Everyone loves getting paid for their efforts, right? Whether you’re running your own show or part of a team, questions about your earnings are bound to pop up. Let’s break it down into simple queries:

- Hourly Paycheck Peek: Wondering how much you make per hour? Let’s find out!

- Salary Sleuthing: Curious about turning your hourly wage into an annual salary? We’ve got you covered.

- Percentage Puzzles: Want to know how long it takes to bump up your income by a certain percentage? We’ve got the formula.

- Payment Predictions: Unsure about what to expect in terms of payment? Let’s figure it out together.

Mehods to Earn $64000 a Year is How Much an Hour?

Guess what? I have two super cool tricks to help you quickly figure out some money questions. These tricks are so easy, you can even show them off at parties and impress everyone with your awesome money skills!

Quick Money Math Trick #1: Turn Hourly into Yearly!

Here’s an easy way to find your yearly salary without breaking a sweat. Just follow these simple steps:

- Take your hourly pay.

- Double it.

- Add a thousand to the end.

For example:

- If you earn $20/hour, you make around $40,000/year. (Double $20 is $40. Add 000 for $40,000.)

- At $25/hour, you’re looking at approximately $50,000/year.

Want to go backward? If you know your yearly salary and want to find your hourly rate:

- Take the yearly amount.

- Divide by two.

- Drop the thousand.

For instance:

- $60,000/year translates to about $30/hour. (Divide $60,000 by 2, drop the 000 for $30!)

Why This Money Trick Rocks! 🚀

There are two fantastic reasons why this money math trick is a game-changer:

- Job Jugglery: Ever had to compare an hourly job with a salaried one (or the other way around) while hunting for new gigs? This trick is your go-to hourly to annual salary calculator.

- Freelance Freedom: If you’re a newbie freelancer unsure about what to charge, this trick’s got your back. Check out salaries for full-time jobs on Google or Glassdoor, convert them to hourly rates, and voila! It’s a handy guide. As you become a pro, remember to up your rates because you’re worth it.

Now, common questions like “How much should I charge?” or “Is $XX/hour too much or too little?” become a breeze. Just peek at your ideal (aka realistic) salary and determine your hourly rate in a snap.

Bonus: Triple Trick Treat! 🎉

If you’re still scratching your head about pricing, try these two extra tricks:

- Double Resentment Number: Figure out the lowest rate that would leave you resentful. Double it, and that’s your starting point (e.g., if $15/hour feels too low, start at $30).

- Google Guru: Simply Google the average hourly rate for your service. It’s like taking a cue from the next guy in the game.

Once you hit that sweet $1,000 milestone, don’t be shy – dial up your prices. There’s no strict rule on how much to charge; it’s your time to shine and tune those rates up! 💸✨

Smart Money Move #2: Master the Rule of 72!

Ever wondered how long it takes to double your money? Here’s the trick: It’s called the Rule of 72.

The Magic Math:

- Take the number 72.

- Divide it by your return rate percentage.

- The answer? The number of years to double your money.

Formula in Action: Let’s say you’re rocking a 10% interest rate from an index fund.

- Divide 72 by 10 (your return rate).

- Result: Approximately 7 years to double your money.

Imagine tossing $5000 into the investment mix today. With a 10% return, you’d be looking at $10,000 in just 7 years. Cool, right?

And here’s the sweet part: It keeps doubling every 7 years, as long as the return rate stays steady. It’s like a money multiplication magic trick! 🎩💰

Why This Money Magic Works Wonders! 🌟

The Rule of 72 isn’t just a cool trick; it’s your ticket to doubling your money without breaking a sweat. Here’s why it’s so awesome:

- Little Turns to Lots: You can watch your investment double by putting in just a bit of money. It’s like money magic in action!

- Real-Life Example: Let me share a heartwarming story. I stashed away $1,000 in an index fund as a gift for a friend’s baby. Assuming a 10% annualized return, check out the growth:

- Age 1: $1,000

- Age 7: $2,000

- Age 14: $4,000

- Age 21: $8,000

- Age 28: $16,000

- Age 35: $32,000

- Age 42: $64,000

- Age 49: $128,000

- Age 56: $256,000

- Age 63: $512,000

- It Grows and Grows: Sure, it’s a simplified model with a 10% return, and we’re not factoring in inflation or taxes. But it proves that even a small $1,000 investment can bloom over time without adding more cash.

- Time, Fees, and Smart Picks: The key factors? Time, minimizing fees and taxes, and choosing sensible, long-term investments.

Now, Your Turn: What’s your money going to do? Sit in a bank account or start making moves in the investment game? The sooner you start, the smoother the road to wealth. This isn’t just talk – over 100 years of stock market evidence backs it up.

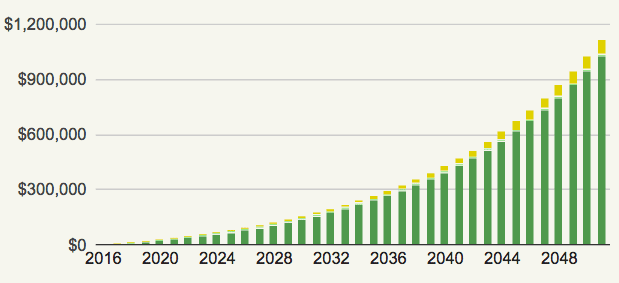

Need More Proof? Here’s a Scenario: If you’re 25 and invest $500/month in a low-cost index fund until you’re 60, how much do you think you’d have? Let’s dive into the numbers and see the magic unfold! 💸🚀

Million-Dollar Magic Unveiled! 💰✨

Guess what awaits you after a bit of clever investing? Drumroll, please… $1,116,612.89! Yes, you can be a millionaire by tossing just a few thousand dollars into the investment mix each year.

Hold up, this isn’t the Hollywood scene with flashy stockbrokers making mega trades and yelling “SELL” for dramatic effect. Nope, it’s all about the smart move – investing in low-cost, diversified index funds consistently. The real magic lies in staying steady, not chasing after wild stocks or strange investments.

Here’s your roadmap to a Rich Life:

- Hourly to Salary Magic: Figure out your rates using the hourly to annual salary trick. It’s your ticket to invest in those index funds.

- Rule of 72 Wizardry: Let the rule of 72 guide you on when your index fund investment could set you up for a comfy retirement.

Read Also: The Rise of Arm Holdings: Dominating the AI Revolution